Algorithmic Stewardship: What Ancient Ethics and Kelly’s Criterion Agree On

How a medieval banking dynasty and a Bell Labs mathematician arrived on the same answer

The Mughals and their Jain Bankers

In the mid-sixteenth century, the Mughal empire was, by some estimates, the largest economy in the world — larger than all of Europe combined. It was institutionally sophisticated, with statistical tracking of agricultural output across ten-year averages, and a multi-ethnic and multi-religious economic system. Jain banking families were a prominent part of this architecture, bringing commercial principles from a tradition already centuries old, emphasizing non-possessiveness and caution about what they could really know.

As the principal in the financial arrangement, the Mughals contributed complementary constraints. Akbar introduced the concept of Akhlaq, or a “Circle of Equity” as a guiding principle in which the bankers helped manage risk while tying together various classes of society and expanding the economy. Production was tracked through the Dahsalah system of ten-year statistical averaging and projection, giving the empire an unusually long planning horizon.

Sovereign-banker relationships in Europe tended toward instability — either the sovereign accumulated unpayable debts and eliminated the banker, or the banker accumulated autonomous power and threatened the sovereign. The Mughal arrangement was architecturally different — mutualistic rather than extractive, and structured so that neither party’s long-term interest was served by defection. Something in its architecture made it last, and part of this may be explained by a mathematical theory of financial risk coming from information theory.

The Mathematics of Risky Outcomes

The theory of probability originated from a mathematical study of monetary outcome of gambling on prop bets. Ironically, betting was considered less morally threatening than study of long-term investments, since risk compounding and potential usurious schemes are avoided. In the mathematical analysis of financial outcomes, investment and gambling are essentially indistinguishable. They differ in other dimensions, however — namely in the side-effect of the transaction and the nature and responsibilities in the relationship between parties.

In the mid-1600s, even as the most famous Jain banking house of Jagat Seth was established on the other side of the world, Pascal and Fermat worked out the mathematics of prop bets. They introduced the concept of the expected value of a proposition: a bet with a 10% chance of getting $100 will pay off $10 on average. Therefore, paying less than $10 for this chance should produce profits on average. This shaped the development of probability theory which has led to our modern notions of economics, with further developments into the microeconomics of an ideal firm, and the macroeconomics of an entire system.

Recently, however, the physicist Ole Peters has suggested that a individualistic point of view has been sorely missing. By centering on expected values over theoretically independent trials, this misses that an individual’s long-term outcomes are based on a sequence of decisions. Specifically the relative size of the investment to your portfolio matters a lot – you could lose all of your money, which would greatly limit your further activity! This thinking takes inspiration from extending basic probability theory with the 20th century development of information theory developed at Bell Labs, leading to a new theory of “ergodicity economics.”

After Shannon’s landmark development of information theory in 1948, it became natural to connect probabilistic processes from various domains across science, including social sciences, to the transmittal of information. Kelly’s paper ‘A New Interpretation of Information Rate’ was published in 1956 and derives a formula for long-term expected accumulation of money assuming a sequence of risky payoffs. Kelly followed the tradition of Pascal and Fermat in formulating his work in terms of the long-term outcomes of a prudent gambler who reserves a certain fraction of his assets, as opposed to a ‘classical gambler.’

Applied to investments, the Kelly criterion captures a long-term perspective on the validity of the policy, but to account for imprecise knowledge of risks a ‘fractional Kelly’ approach is typically used which reduces exposure from the Kelly optimal point for improved liquidity and lower volatility. Kelly’s criterion fundamentally is about geometric survival under uncertainty — not about maximizing expected return. It uses p, the probability of success, u, the payoff for a success, d, the loss on failure, and f, the fraction of wealth invested in the following formula for growth rate:

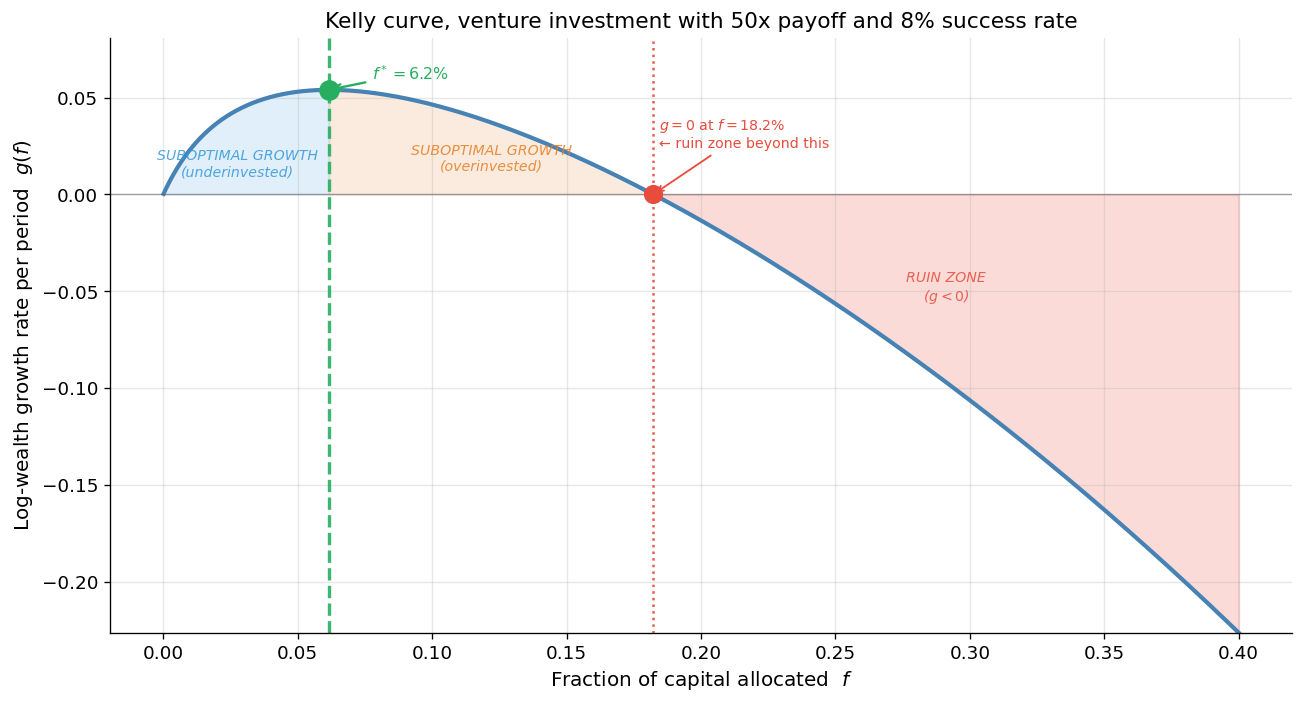

The following figure depicts the Kelly growth curve for an example of an investment opportunity that is evocative of a hot Silicon Valley startup. It has an 8% chance of success, but, if successful, will return 50x on the investment and otherwise will go bust. The Kelly analysis indicates what we all know to be true – a prudent investor should account for their analysis of the company and their own situation.

The at-Kelly optimal point of maximal growth is 6.2% of the portfolio invested, with regions of under-Kelly (sub-optimal), and a ruin zone above 18.2% investment. The mathematics predicts that consistently investing 20% into such ‘gold mine’ opportunities will eventually result in losing all of your money. In practice, the overall portfolio volatility can potentially generate uncomfortable losses at the Kelly optimal point, so it’s prudent to operate in a ‘fractional Kelly’ zone which still captures most of the growth – say an allocation closer to 4% in the example shown. Interestingly, the Jagat Seth, operating without this mathematics, had nevertheless institutionalized many of these conclusions as intuitions.

Note that the Kelly fraction is zero when there is no edge – that is, the expected ROI is not greater than 1. Thus, whether it is a lotto ticket or speculating without a reasonable expectation of gain, the recommended course of action is to pass on the investment. Technically, the risk underwriting (8% probability of success) and the payoff prediction (50x return) require skill to approximate. So, the fractional Kelly approach also acts as a hedge to approximation errors.

Convergence of moral principles and Kelly’s criterion

The principles of Jain banking were guided by spiritual belief, as documented by Jain śrāvakācāra literature which made religious principles a cornerstone in commercial life. A focus on Karmic time horizons brings a balance between transaction outcomes with the overall long-term trajectory. Kelly’s criterion, derived from information theory, reaches the same conclusion by a different route: the correct unit of analysis is not expected return on a single bet but geometric survival across repeated risk exposure.

Similarly, the principle of Anekantavada (many-sidedness) encourages an epistemic humility about edge — which points to fractional Kelly as intuitive virtue, not just math. Another key principle is that of Aparigraha (non-possessiveness), which further gives a philosophical justification against over-betting. It also helped establish a trusting and sustainable principal-agent relationship with the Mughals — a mutualistic and no-debt-trap political dynamic.

Kelly’s criterion describes, in the language of information theory, why this kind of architecture is structurally stable: size positions with humility about your edge, cap exposure below the threshold where ruin becomes inevitable regardless of expected return, allocate nothing to propositions without genuine edge. The Jagat Seth arrangement exhibited these properties.

Algorithmic Stewardship

Since mathematics is abstract, it is generally considered the furthest thing from moral philosophy. However, the application of mathematics can reflect opinions and morals. Focusing on the long term is a key aspect of stewardship of resources: on behalf of others or the future. This suggests that this correspondence between ethical principles and long-run mathematics is not just a historical curiosity, but can motivate new approaches for the future.

Finance is now largely brokered through digital infrastructure. Human judgment, increasingly, must operate through policies and algorithms rather than direct assessment. One example lies in the prevalence of high-frequency trading algorithms in equities markets, which today vastly outweighs the volume of direct human-initiated trades other than in rare niches. The idea that people are mediated through algorithms is not a new idea, and it represents a substantial innovation, just as the Hundi banking system in medival India and Letters of Credit in medival Europe mediated trade on a vast scale.

This points to a potential need for algorithmic encoding of stewardship, beyond efficient transactions. Indeed, algorithmic trading platforms exist, and current technology trends would indicate that these algorithms may become more agentic and long-running. Encoding qualities of stewardship would engender trustworthiness, and ideas like Kelly’s criterion could potentially provide guidance by mathematical policies rather case-by-case analysis. The algorithmic approach provides precision and some measure of consistency with standing policies — repeatable rules that produce stability when followed consistently across time. The behavioral convergence of rules like Kelly’s criterion to age-old ethical philosophies becomes a path towards building confidence in algorithmic decision-making for stable, equitable outcomes.

Kelly’s criterion only addresses the question of allocation amount. What constitutes a legitimate use of capital in the first place is not captured in the analysis. It requires an ethical pre-filter to select what investments are valuable in the first place. Things like “ESG whitelists” offer easy integration but have been critiqued for being inaccurate or arbitrary (e.g. giving oil companies higher ESG scores than green energy). The more fundamental challenge — algorithmically encoding what counts as equitable in the first place — remains an open problem.

The modern complex and information rich world is impractical without scalable approaches to decision-making. However, this analysis shows that sustainability can scale, without the need to blindly focus on short-term outcomes. Wherever decisions compound over time — portfolios, institutions, resource extraction — the question is the same. Not whether one particular idea pays off, but whether the policy protects survivability while being open to good ideas. Collective over-betting assumes someone else absorbs the ruin. On a closed system, there is no someone else.